The Frontier Is a Commute

The entire Western AI frontier fits inside a single Bay Area commute. This should concern every security planner.

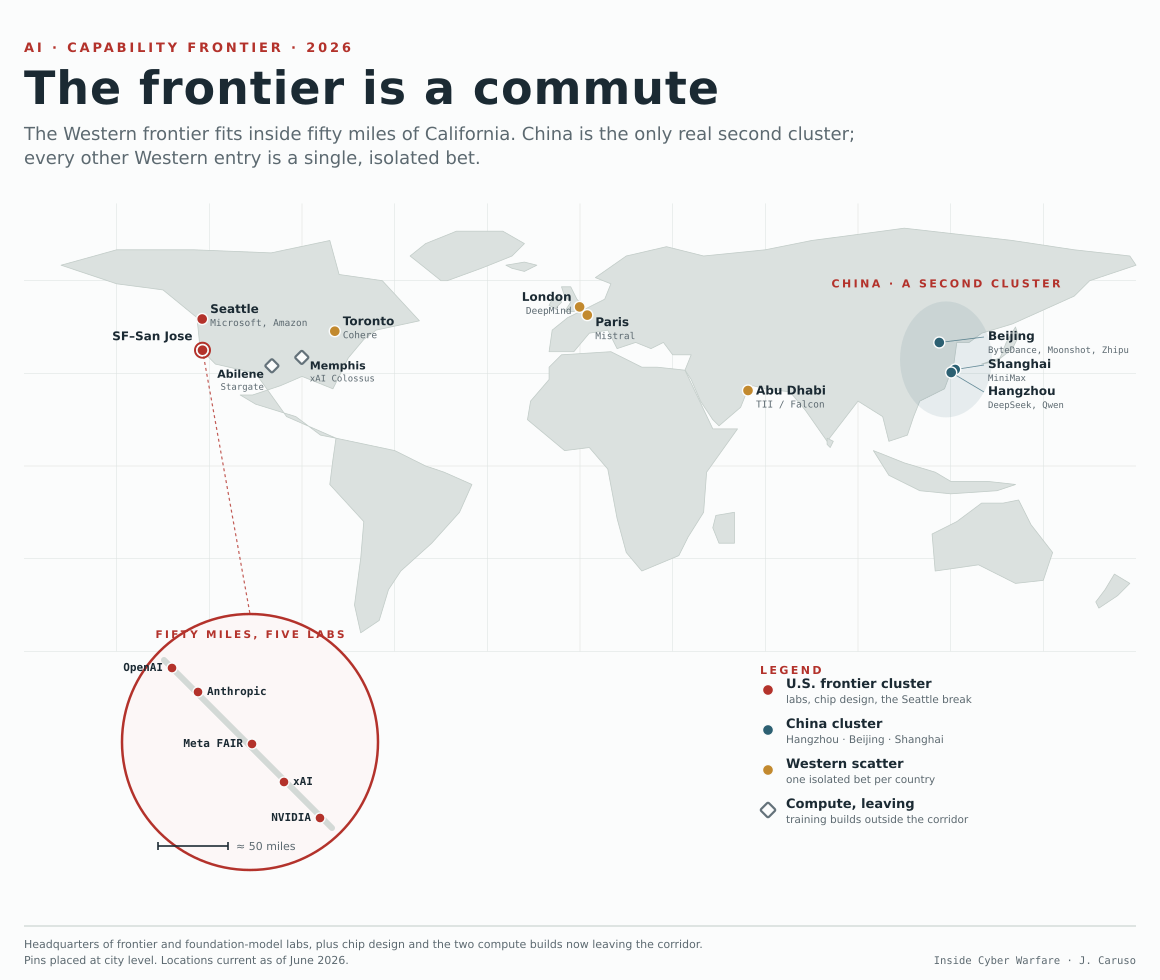

Plot the headquarters of the companies that define artificial intelligence, and the pattern is obvious before you finish dropping the pins. The part of the industry that sets the capability frontier sits in a strip of California roughly fifty miles long, San Francisco to San Jose. Remove China from the picture and nearly the entire Western frontier falls inside that corridor. Seattle is the only domestic exception.

Why that matters depends on what “matter most” means. The public conversation is rarely precise about it.

“AI company” is not a category

The industry gets flattened into one label, and that label is useless for thinking about risk. AI is a stack. The layers are not interchangeable.

At the top by capability, not by headcount or valuation, sit the frontier labs. The term has a precise meaning that casual usage erodes. A frontier lab trains its own foundation models from scratch, on the order of tens of thousands of accelerators running for weeks or months. It operates at the current capability boundary, not behind it. And it produces the architectural advances that everyone downstream inherits. By that definition the global count is small. Under twenty labs, plausibly fewer.

Everything else descends from that layer. Foundation-model labs train real models below the frontier, often open-weight and domain-specific. Fine-tuners take an existing base model and reshape it for a vertical (law, code, clinical data) using a fraction of the original compute. The application layer, where most of the named “AI companies” live, rents intelligence through an API and builds product on top of it. Beneath all of it runs the infrastructure: compute, model-serving, the data pipelines. The frontier labs depend on that infrastructure as heavily as anyone above them.

The strategically decisive layer is the first one. Capability originates there and diffuses downward. Its geography is what should concern a security planner.

Where the frontier sits

The corridor is dense. OpenAI and Anthropic in San Francisco. Meta’s FAIR in Menlo Park. xAI in Palo Alto. The chip-design and model-serving layer sits in the same handful of zip codes: NVIDIA in Santa Clara, the serving firms in San Francisco and San Mateo. So does the established software that consumes frontier output, from Salesforce to GitHub to Adobe. Seattle, with Microsoft and Amazon, is the only real break in the pattern, and it is still a single metro. One layer has started to leave. Raw compute is moving to where the power and land are, xAI’s Colossus to Memphis, the Stargate build to Abilene. Capital and silicon disperse when they have to. The talent and the IP have not.

Abroad, the Western frontier is not a cluster. It is a scatter of one-per-country bets. Google DeepMind in London. Mistral in Paris. Cohere in Toronto. Falcon, out of the Technology Innovation Institute in Abu Dhabi. Each is its nation’s single entry at the frontier. Europe’s entire frontier presence comes down to two cities.

China is the exception to the scatter. Hangzhou anchors DeepSeek and Alibaba’s Qwen. Beijing holds ByteDance, Moonshot, and Zhipu. Shanghai adds MiniMax. That is depth, and planned resilience.

Concentration of Resources is a Tactical Blunder

Concentration is fragility, and the warning usually arrives before the failure. Through the 1930s the U.S. Pacific Fleet operated out of West Coast ports. In 1940, to signal resolve to Japan, the Roosevelt administration ordered it consolidated forward to Pearl Harbor and held it there. Admiral James Richardson, the Navy’s foremost authority on Pacific warfare, told Roosevelt directly and then put it in writing: a fleet massed in one exposed harbor was the logical first target in a war with Japan. He was relieved of command for pressing it. The administration wanted a deterrent. What it built was a target, and the officer best placed to see it was removed for saying so.

The frontier carries the same shape. A capability that lives in one seismic zone, on one regional power grid, inside one metropolitan labor market is efficient. It is not resilient. The talent and the intellectual property that define it aren’t just co-located in a country. They are co-located in a commute. Any planner who has war-gamed single-point-of-failure problems will recognize the target.

Geography narrows the collection problem. A distributed industry is a hard target. A frontier that resolves to a small number of buildings and a small, mobile talent pool is a legible one. Legible to foreign intelligence services, to insider threat, to the ordinary churn of people carrying what they know from one lab to another just a few exits away. Concentration compresses them into an adversary’s target set.

We are measuring the wrong contest. The dominant frame treats AI as a race to a finish line: who crosses the capability threshold first. The map argues for a different metric. The durable advantage is depth and the resilience of where capability physically sits. That’s what China has been building. The U.S. may win the velocity race, but China wins on survivability.

None of this argues for dispersing the frontier by fiat. The clustering exists because proximity compounds talent and capital, and that effect is real. But the security community assumes the competition is about capability gaps and compute access. The geography points to a quieter variable: concentration itself. The side with a true second cluster has an answer to a question we have not seriously asked.

The frontier is a commute. That should be in the threat model.

Worldwide Lab Reference Data By Tier

Tier 1: Frontier Labs

United States

OpenAI — San Francisco, CA

Anthropic — San Francisco, CA

Google DeepMind — London, UK (with Mountain View operations)

Meta AI / FAIR — Menlo Park, CA

xAI — Palo Alto, CA

Amazon (Nova/Titan) — Seattle, WA

Microsoft Research — Redmond, WA

China

DeepSeek — Hangzhou

Alibaba / Qwen — Hangzhou

ByteDance / Seed — Beijing

Moonshot AI — Beijing

Zhipu AI — Beijing

MiniMax — Shanghai

Rest of world

Mistral — Paris, France

Cohere — Toronto, Canada

TII / Falcon — Abu Dhabi, UAE

Samsung Research — Seoul, South Korea

Tier 2: Foundation Model Labs (Non-Frontier)

Stability AI — London, UK

EleutherAI — distributed/no fixed HQ (open research collective)

BAAI / WuDao — Beijing, China

Hugging Face — Brooklyn, NY (the open-model hub; also straddles infrastructure)

Tier 3: Fine-Tuners & Derivative Builders

This is the most geographically diffuse tier by design — it’s thousands of domain shops fine-tuning someone else’s base model. The headline example we used is Cursor / Anysphere (San Francisco), which fine-tuned Kimi K2.5 into Composer 2. Most of this tier is enterprise and vertical shops that don’t register as “AI companies” on a map.

Tier 4: AI Application Companies

Salesforce (Einstein) — San Francisco, CA

GitHub Copilot (Microsoft) — San Francisco, CA

Adobe (Firefly) — San Jose, CA

Perplexity — San Francisco, CA (RAG-based search, application layer)

Infrastructure (beneath everything)

NVIDIA — Santa Clara, CA (compute)

Together AI — San Francisco, CA (model serving)

Fireworks AI — San Mateo, CA (serving; the Cursor/Kimi intermediary)

Scale AI — San Francisco, CA (data/RLHF pipeline)

Pinecone — New York, NY (vector DB)

Weaviate — Amsterdam, Netherlands (vector DB)